Uranium is a relatively common metal, found in rocks and seawater. Economic concentrations of it are not uncommon.

Its availability to supply world energy needs is great both geologically and because of the technology for its use.

Quantities of mineral resources are greater than commonly perceived.

The world’s known uranium resources increased by at least one-quarter in the last decade due to increased mineral exploration.

Uranium is a relatively common element in the crust of the Earth (very much more than in the mantle). It is a metal approximately as common as tin or zinc, and it is a constituent of most rocks and even of the sea.

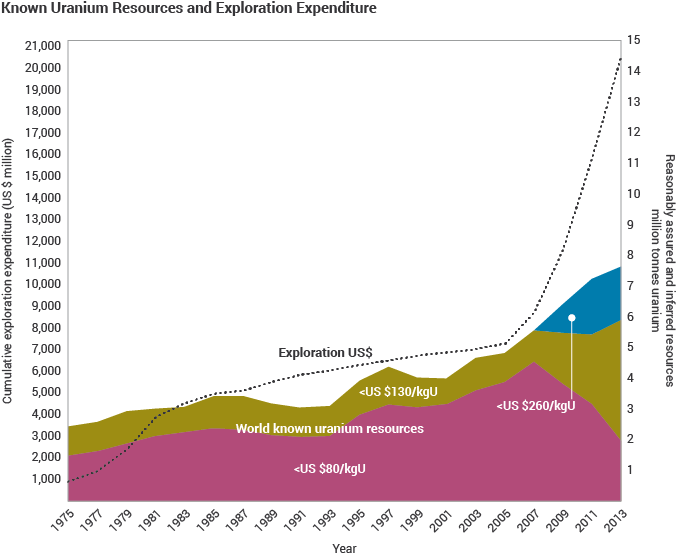

Current usage is about 63,000 tU/yr. Thus the world’s present measured resources of uranium (5.7 Mt) in the cost category less than three times present spot prices and used only in conventional reactors, are enough to last for about 90 years. This represents a higher level of assured resources than is normal for most minerals. Further exploration and higher prices will certainly, on the basis of present geological knowledge, yield further resources as present ones are used up.An initial uranium exploration cycle was military-driven, over 1945 to 1958. The second cycle was about 1974 to 1983, driven by civil nuclear power and in the context of a perception that uranium might be scarce. There was relatively little uranium exploration between 1985 and 2003, so the significant increase in exploration effort since then could conceivably double the known economic resources despite adjustments due to increasing costs. In the two years 2005-06 the world’s known uranium resources tabulated above and graphed below increased by 15% (17% in the cost category to $80/kgU). World uranium exploration expenditure is increasing, as the the accompanying graph makes clear. In the third uranium exploration cycle from 2004 to the end of 2013 about US$ 16 billion was spent on uranium exploration and deposit delineation on over 600 projects. In this period over 400 new junior companies were formed or changed their orientation to raise over US$ 2 billion for uranium exploration. Much of this was spent on previously-known deposits. All this was in response to increased uranium price in the market and the prospect of firm future prices.The price of a mineral commodity also directly determines the amount of known resources which are economically extractable. On the basis of analogies with other metal minerals, a doubling of price from present levels could be expected to create about a tenfold increase in measured economic resources, over time, due both to increased exploration and the reclassification of resources regarding what is economically recoverable.This is in fact suggested in the IAEA-NEA figures if those covering estimates of all conventional resources (U as main product or major by-product) are considered – another 7.3 to 8.4 million tonnes (beyond the 5.9 Mt known economic resources), which takes us past 200 years’ supply at today’s rate of consumption. This still ignores the technological factor mentioned below. It also omits unconventional resources (U recoverable as minor by-product) such as phosphate/ phosphorite deposits (up to 22 Mt U), black shales (schists – 5.2 Mt U) and lignite (0.7 Mt U), and even seawater (up to 4000 Mt), which would be uneconomic to extract in the foreseeable future, although Japanese trials using a polymer braid have suggested costs a bit over $600/kgU. US work has developed this using polyethylene fibres coated with amidoxime, which binds uranium so that it can be stripped with acid. Research proceeds.

It is clear from this Figure that known uranium resources have increased almost threefold since 1975, in line with expenditure on uranium exploration. (The decrease in the decade 1983-93 is due to some countries tightening their criteria for reporting. If this were carried back two decades, the lines would fit even more closely. Since 2007 some resources have been reclassified into higher-cost categories.) Increased exploration expenditure in the future is likely to result in a corresponding increase in known resources, even as inflation increases costs of recovery and hence tends to decrease the figures in each cost category.

Reactor fuel requirements

The 230 t amount is equivalent to about six reloads for a 1000 MWe reactor.

The world’s power reactors, with combined capacity of some 375 GWe, require about 68,000 tonnes of uranium from mines or elsewhere each year. While this capacity is being run more productively, with higher capacity factors and reactor power levels, the uranium fuel requirement is increasing, but not necessarily at the same rate. The factors increasing fuel demand are offset by a trend for higher burn-up of fuel and other efficiencies, so demand is steady. (Over the years 1980 to 2008 the electricity generated by nuclear power increased 3.6-fold while uranium used increased by a factor of only 2.5.)Reducing the tails assay in enrichment reduces the amount of natural uranium required for a given amount of fuel. Reprocessing of used fuel from conventional light water reactors also utilises present resources more efficiently, by a factor of about 1.3 overall.The 2014 Red Book said that efficiencies on power plant operation and lower enrichment tails assays meant that uranium demand per unit capacity was falling, and the report’s generic reactor fuel consumption was reduced from 175 tU per GWe per year at 0.30% tails assay (2011 report) to 160 tU per GWe per year at 0.25% tails assay (2016 report). The corresponding U3O8 figures are 206 tonnes and 189 tonnes. Note that these figures are generalisations across the industry and across many different reactor types.Today’s reactor fuel requirements are met from primary supply (direct mine output – 78% in 2009) and secondary sources: commercial stockpiles, nuclear weapons stockpiles, recycled plutonium and uranium from reprocessing used fuel, and some from re-enrichment of depleted uranium tails (left over from original enrichment). These various secondary sources make uranium unique among energy minerals.

Nuclear weapons as a source of fuel

An important source of nuclear fuel is the world’s nuclear weapons stockpiles. Since 1987 the United States and countries of the former USSR have signed a series of disarmament treaties to reduce the nuclear arsenals of the signatory countries by approximately 80 percent.The weapons contained a great deal of uranium enriched to over 90 percent U-235 (i.e. up to 25 times the proportion in reactor fuel). Some weapons have plutonium-239, which can be used in mixed-oxide (MOX) fuel for civil reactors. From 2000 the dilution of 30 tonnes of military high-enriched uranium has been displacing about 10,600 tonnes of uranium oxide per year from mines, which represents about 15% of the world’s reactor requirements.Details of the utilisation of military stockpiles are in the paper Military warheads as a source of nuclear fuel.

Other secondary sources of uranium

The most obvious source is civil stockpiles held by utilities and governments. The amount held here is difficult to quantify, due to commercial confidentiality. At the end of 2014 some 217,000 tU total inventory was estimated for utilities – USA 45,000 t, EU 53,000 t, China 74,000 t, other East Asia 45,0000 t (World Nuclear Association 2015 Nuclear Fuel Report). These reserves are expected to be drawn down somewhat, but they will be maintained at a fairly high level to to provide energy security for utilities and governments.

Recycled uranium and plutonium is another source, and currently saves 1700-2000 tU per year of primary supply, depending on whether just the plutonium or also the uranium is considered. This is expected to rise to 3000-4000 tU/yr by 2020. In fact, plutonium is quickly recycled as MOX fuel, whereas the reprocessed uranium (RepU) is mostly stockpiled, and the inventory at the end of 2014 was estimated at 75,000 tU.

Re-enrichment of depleted uranium (DU, enrichment tails) is another secondary source. There is about 1.3 million tonnes of depleted uranium available, from both military and civil enrichment activity since the 1940s, most at tails assay of 0.25-0.35% U-235 (though the USA has 114,000 tU assaying 0.34% or more). Non-nuclear uses of DU are very minor relative to annual arisings of over 40,000 tU per year. This leaves most DU available for mixing with recycled plutonium on MOX fuel or as a future fuel resource for fast neutron reactors. However, some that has relatively high assay can be fed through under-utilised enrichment plants to produce natural uranium equivalent, or even enriched uranium ready for fuel fabrication. Russian enrichment plants have treated 10-15,000 tonnes per year of DU assaying over 0.3% U-235, stripping it down to 0.1% and producing a few thousand tonnes per year of natural uranium equivalent. This Russian program treating Western tails has now finished, but a new US one is expected to start when surplus capacity is available, treating about 140,000 tonnes of old DU assaying 0.4% U-235.

Underfeeding at enrichment plants is a significant source of secondary supply, especially since the Fukushima accident reduced enrichment demand for several years. This is where the operational tails assay is lower than the contracted/transactional assay, and the enricher sets aside some surplus natural uranium, which it is free to sell (either as natural uranium or as enriched uranium product) on its own account. UxC estimates that with an optimum tails assay of 0.23% in 2013, the enrichers have the potential to contribute up to 7700 tU per year to world markets by underfeeding. The 2015 edition of the World Nuclear Association’s Nuclear Fuel Report estimates 5000 to 8000 tU/yr from this source to the mid-2020s.

Thorium as a nuclear fuel

Today uranium is the only fuel supplied for nuclear reactors. However, thorium can also be utilised as a fuel for CANDU reactors or in reactors specially designed for this purpose. Neutron efficient reactors, such as CANDU, are capable of operating on a thorium fuel cycle, once they are started using a fissile material such as U-235 or Pu-239. Then the thorium (Th-232) atom captures a neutron in the reactor to become fissile uranium (U-233), which continues the reaction. Some advanced reactor designs are likely to be able to make use of thorium on a substantial scale.The thorium fuel cycle has some attractive features, though it is not yet in commercial use. Thorium is reported to be about three times as abundant in the earth’s crust as uranium. The 2009 IAEA-NEA Red Book lists 3.6 million tonnes of known and estimated resources as reported, but points out that this excludes data from much of the world, and estimates about 6 million tonnes overall.

Main references

OECD NEA & IAEA, 2014, Uranium 2014: Resources, Production and Demand

WNA 2013, The Global Nuclear Fuel Market – Supply and Demand 2013-2030

UN Institute for Disarmament Research, Yury Yudin (ed) 2011, Multilateralization of the Nuclear Fuel Cycle – The First Practical Steps

Monnet, A, CEA, Uranium from Coal Ash: Resource assessment and outlook, IAEA URAM 2014